How Instarem Business Card helps businesses save on FX and fees

This article covers:

- Key takeaways

- FX rates and fees hurt more than businesses realise

- Where the costs add up with traditional bank cards

- Introducing Instarem’s Business Card

- Who benefits the most from Instarem’s Business Card?

- Final thoughts: Unlock savings on FX rates and fees with Instarem

- FAQs about Instarem’s Business Card

Key takeaways

- FX markups and foreign transaction fees can quickly add up, reducing business profit margins.

- Instarem Business Card offers competitive FX rates with transparent pricing.

- Real-time visibility and spend controls help prevent overspending and policy breaches.

- The Instarem Business Card runs on the Mastercard network, providing global acceptance with cost efficiency.

Small and medium enterprises (businesses) that transact frequently in foreign currencies know how FX markups and hidden fees can quietly erode profits. What seems minor, such as extra charges on subscriptions or overseas vendor payments, can accumulate significantly over time.

For businesses operating on tight margins, these costs matter. When left unchecked, they reduce profitability and limit resources that could otherwise be invested in growth. That is why choosing the right financial tools is critical.

Instarem Business Card gives businesses a smarter way to manage cross-border spending. With competitive exchange rates, transparent pricing, and full control over corporate expenses, businesses can reduce unnecessary costs while maintaining oversight.

Here’s how Instarem Business Card helps you lower FX costs, avoid hidden fees, and manage international spending more efficiently.

FX rates and fees hurt more than businesses realise

Many businesses rely on traditional bank-issued cards without fully understanding how FX markups and foreign transaction fees are applied. Over time, these additional charges can quietly chip away at already tight margins.

The hidden cost of convenience

Traditional banks offer familiarity and wide acceptance. However, behind that convenience, costs are often embedded in exchange rates and transaction fees.

Banks typically apply FX markups on top of card network or interbank rates. They may also charge foreign transaction fees. While each charge may appear small, together they inflate operational expenses month after month.

Common scenarios that trigger FX losses

Foreign currency spending is rarely occasional. For many businesses, it is a routine part of business operations. Common examples include:

Overseas supplier or freelancer payments

Suppliers and freelancers often invoice through online platforms. Businesses frequently use corporate cards for fast, convenient settlement.

Software subscriptions

Accounting software, CRM systems, cloud platforms, and productivity tools are often billed monthly in foreign currencies. Corporate cards are the easiest way to manage these payments.

Online advertising

Digital advertising is essential for growth. Funding ad spend through corporate cards is quick and straightforward, but FX costs can accumulate.

International travel and accommodation

Flights, hotels, and travel-related expenses are commonly charged to corporate cards to avoid reimbursements. Cross-border transactions can result in additional FX charges.

Where the costs add up with traditional bank cards

Familiarity and convenience keep many businesses tied to traditional bank cards. However, behind the simplicity, businesses may be paying more than necessary.

FX markups

Traditional banks typically add a margin to card network exchange rates. For example, while the mid-market rate between SGD and USD may be published publicly, banks often apply an additional markup.

These margins vary by bank and are not always clearly disclosed. Over time, recurring transactions amplify these hidden costs.

Risk of double conversion

Double conversion can occur when the transaction currency, card currency, and merchant settlement currency differ.

For instance, a subscription priced in USD may be converted into SGD by the card issuer, then converted again during settlement. Each conversion may include its own markup, increasing total costs.

Foreign transaction fees

Many banks charge foreign transaction fees ranging from 1% to 3% per transaction.

For businesses making frequent international payments, this becomes a recurring expense that steadily reduces margins.

Monthly or annual card fees

Traditional bank cards often come with recurring annual or monthly fees. While these may seem routine, they represent ongoing costs simply for maintaining access to the card.

Delayed visibility

Delayed transaction visibility may not directly create fees, but it increases risk. Without real-time data, businesses may overspend, duplicate payments, or face reconciliation delays.

Over time, this adds administrative burden and reduces financial control.

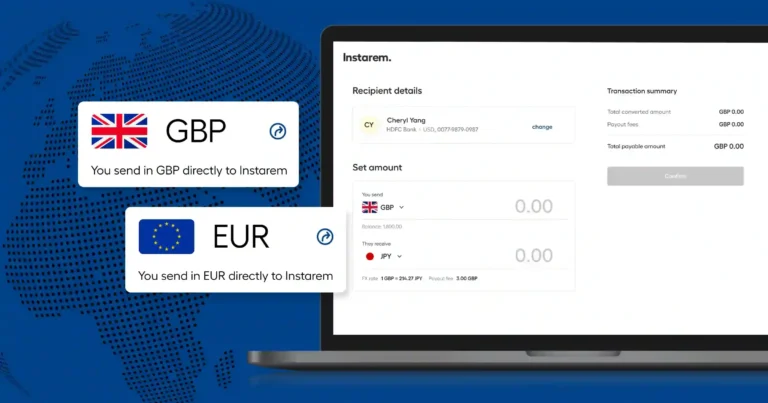

Introducing Instarem’s Business Card

Instarem Business Card is a debit card linked directly to your Instarem Business Account. It enables businesses to fund everyday transactions, including foreign currency payments, with centralised visibility.

Businesses can issue multiple virtual and physical cards and assign them to specific teams, projects, or expense categories.

With competitive FX rates and transparent pricing, the card offers a cost-efficient alternative to traditional bank cards.

How does it work in practice?

Pricing structure set by Instarem — transparent and predictable

FX rates for card transactions follow Instarem’s pricing structure, not traditional bank card pricing.

Because the Business Card is linked to your Instarem account, currency conversion happens at checkout, with fees disclosed upfront. This reduces the likelihood of unexpected post-settlement charges.

For businesses with recurring foreign currency expenses, this transparency makes budgeting more predictable and manageable.

Savings beyond competitive FX rates

Instarem allows businesses to issue multiple virtual cards at no cost. Physical cards incur a one-time issuance fee of SGD 5 per card.

By paying directly with the Business Card, businesses can also reduce reimbursements and manual processing, lowering the risk of administrative errors.

Real-time spend control

All card transactions are consolidated into a single dashboard, providing real-time visibility across the organisation.

Instarem also offers built-in controls:

- Multiple virtual cards: Create cards for specific teams, vendors, or projects.

- Custom spending limits: Set maximum limits per card to maintain budget discipline.

- Instant freeze or cancellation: Freeze or cancel cards immediately in case of misuse or suspicious activity.

For businesses, these controls help align spending with internal policies while simplifying month-end reconciliation.

Global acceptance without compromise

Instarem Business Card operates on the Mastercard network and supports spending in over 100 currencies globally.

Common use cases include:

- SaaS subscriptions

- Digital advertising platforms

- Travel bookings

- Vendor payments that accept card payments

Virtual cards are ideal for online payments, while physical cards can be used for travel or in-store transactions. Currency conversion occurs at checkout with costs disclosed transparently.

Operational efficiency as a cost-saving lever

Operational efficiency is often overlooked as a cost-saving tool.

With all transactions captured automatically in one dashboard, finance teams spend less time reconciling expenses and managing reimbursements.

Clearer visibility enables better decisions, whether cancelling unused subscriptions, renegotiating vendors, or planning foreign currency exposure more carefully.

Who benefits the most from Instarem’s Business Card?

Businesses with regular international spending

Businesses that frequently pay overseas vendors, freelancers, or software subscriptions can benefit from more competitive FX pricing and transparent fees.

Centralised visibility ensures spending remains controlled without requiring complex enterprise systems.

Digital-first companies using global SaaS tools

Many SaaS platforms are billed in foreign currencies. Over time, FX markups and transaction fees increase overall subscription costs.

Instarem Business Card helps keep recurring payments predictable while giving finance teams better oversight.

Businesses with overseas vendors

Vendor payments are often recurring and FX-sensitive. Choosing a more cost-efficient payment solution reduces unnecessary markups and improves financial planning.

Final thoughts: Unlock savings on FX rates and fees with Instarem

A business card with competitive FX rates and transparent pricing can significantly improve cost control.

For businesses that transact regularly in foreign currencies, reducing FX markups and transaction fees helps protect margins and free up budget for growth.

Choosing Instarem Business Card provides access to predictable pricing, global acceptance, and real-time spend control.

Interested in reducing FX costs and improving visibility? Get started by signing up for an Instarem Business Account today.

FAQs about Instarem’s Business Card

Is Instarem’s Business Card a debit or credit card?

Instarem Business Card is a debit card. Transactions are deducted directly from your available balance in the linked Instarem Business Account.

Does the Instarem Business Card replace bank transfers to overseas suppliers?

No. The Business Card is designed for card-based payments. For bank transfers to overseas suppliers, you can use Instarem’s international remittance service.

How are FX rates applied when using the card?

Currency conversion follows Instarem’s pricing structure. FX rates and applicable fees are disclosed at checkout, offering greater transparency compared to traditional bank cards.

Can I control how much is spent on each card?

Yes. You can:

- Set spending limits per card

- Issue virtual cards for specific purposes

- Freeze or cancel cards instantly

These controls help reduce unauthorised use and maintain budget discipline.